Projected to reach a global market value of more than $12.5B by 2026, lending is one of the largest industries within the financial sector.

Yet, with success comes greater risk, and lenders are no strangers to the threat of fraud.

Lending fraud is a prevalent issue worldwide and affects lenders of all kinds, from large banks to small community operations and credit unions — and even Fintechs.

Not only this, but fraudulent activity can stem from both individual consumers and businesses.

One study uncovered that small business lending fraud has increased by 6.9% since 2020. Meanwhile, PwC’s Global Economic Crime and Fraud Survey 2022 revealed that 51% of the 1,200+ survey respondents had experienced fraud at their organization in the past two years — the highest incident level PwC has seen in the last 20 years.

The reality is that fraud is not an issue lenders can afford to ignore.

To overcome the challenge of fraud and keep customers protected, the first key step for lenders is to know which types are most prevalent in the lending industry.

Lending fraud 101: 3 types of fraud you need to know

In general, there are three main types of lending fraud that lenders are facing, each depending on who is willingly engaged in the malicious activity: first-, second- and third-party fraud.

1. Personal loan fraud (first-party loan fraud)

Personal loan fraud is a type of first-party fraud in which the information used belongs to the bad actor themselves –– they simply provide false or exaggerated financial data to a lender. As a result, the person may be approved for a loan they do not actually qualify for.

2. Straw buyer fraud (second-party loan fraud)

Straw buyer fraud involves two parties: the fraudster themselves and a second person (the “straw buyer”) who willingly provides their personal information for a loan application. An example of this is when a straw buyer uses their superior credit rating to apply for a mortgage, but someone else then controls and occupies the property. In this case, the straw buyer often gets financial compensation from the fraudster.

3. Identity theft (third-party loan fraud)

Third-party loan fraud is basically identity theft, a crime in which a fraudster steals personal information from an unwilling victim. A common practice in identity theft is to apply for a loan under someone else’s name and information, receive the loan payout, and then never pay it back. As a result, both the lender and the victim experience significant financial harm, making identity theft one of the most dangerous forms of lending fraud. And it’s bound to become even more of an issue, with sophisticated fraudsters increasingly exploiting tech vulnerabilities arising from the digitalization of the financial industry.

What is the impact of fraud on lenders?

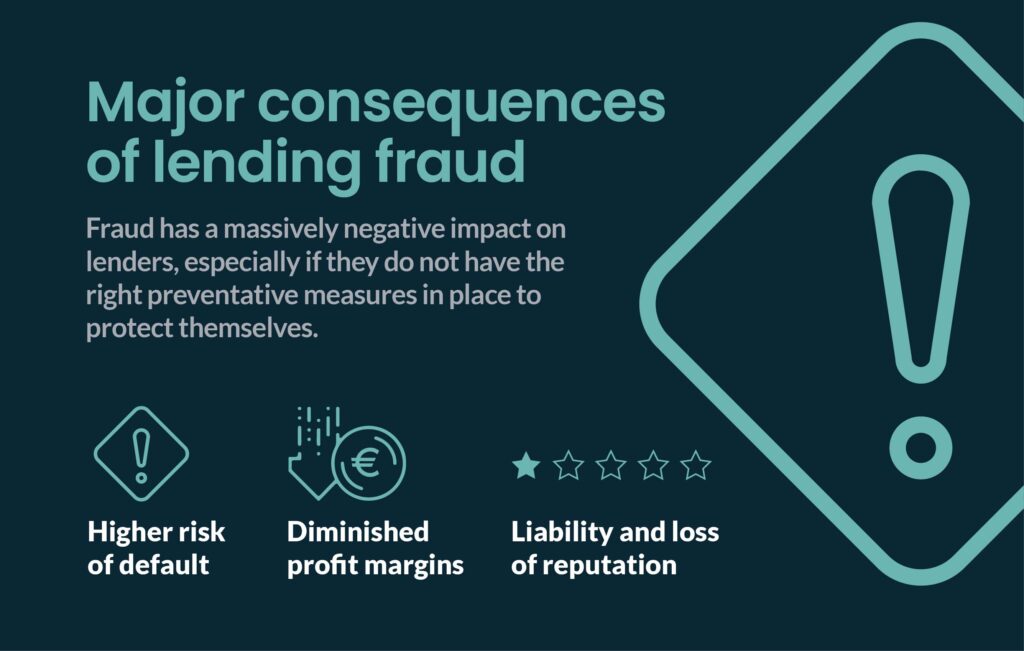

Fraud has a massively negative impact on lenders, especially if they do not have the right preventative measures in place to protect themselves.

Three major consequences of lending fraud include:

Higher risk of default

Lending fraud leads to a much higher risk of default. In the case of first- and second-party fraud, there might be a genuine intention to repay the loan. However, due to the fraudulent manner in which it was obtained, lenders still face a higher probability of loan default. What’s even worse, though, is third-party fraud. Here, the loan taker has no plans whatsoever to repay it, meaning it almost certainly never will be.

Diminished profit margins

While a higher risk of default leads to more non-payments and thus directly lowers revenues, the resulting cost implication also affects lenders’ profits. That’s because whenever there is a default, lenders have to reallocate time, resources, and staff to carry out the often complex process. This is particularly risky for lenders that offer unsecured loans, who would end up having to write the default off as a loss if the funds cannot be recovered. And even if loans are secured by particular assets, depending on the severity of loan fraud, these may actually not be (fully) enforceable. For instance, if an asset doesn’t exist, is overvalued, or is not under the debtor’s ownership.

Lender liability and loss of reputation

If a customer turns out to be a victim of fraud, a lender is at risk of facing a lender liability lawsuit or other region-specific legal troubles. This is especially true if the fraud incident occurred due to a lack of proper risk mitigation on the lender’s behalf. Due to the nature of the lending industry, the resulting negative PR impact, brand damage, and loss of customer trust can also lead to decreased future business opportunities and loyalty.

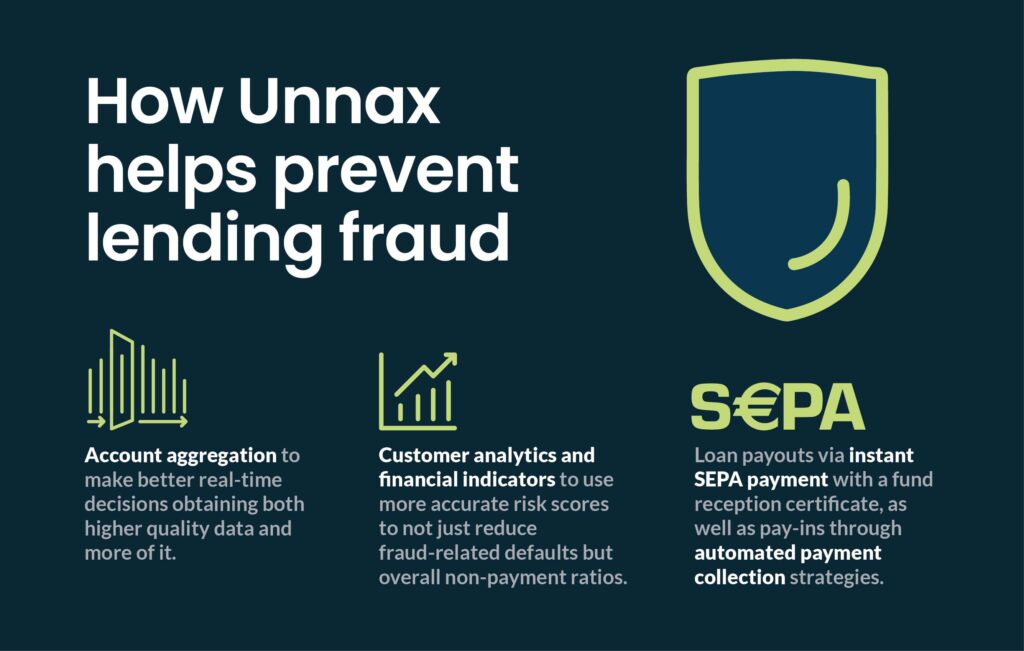

Final thoughts: How Unnax helps prevent lending fraud

The best way to limit lending fraud is to create more accurate loan application profiles. At Unnax, we help lenders do exactly that by offering three key solutions:

- Utilizing account aggregation to make better real-time decisions, thanks to obtaining both higher quality data and more of it. This allows lenders to see the loan applicant’s true and full financial situation.

- Enhancing applicants’ lending profiles with superior customer analytics and financial indicators, enabling lenders to use more accurate risk scores to not just reduce fraud-related defaults but overall non-payment ratios.

- Improving payments, including loan payouts via instant SEPA payment and with a fund reception certificate, as well as pay-ins through automated payment collection strategies.

Talk to our sales team today to learn how Unnax can fortify your lending firm against fraud.